For people of faith, generosity is not just a financial choice but a spiritual one – rooted in stewardship and the joy of giving back. As we approach the end of another year, charitable giving is likely top of mind. There are many ways to give back, each with unique benefits and considerations. One practical tool is the Individual Retirement Account (IRA).

For people of faith, generosity is not just a financial choice but a spiritual one – rooted in stewardship and the joy of giving back. As we approach the end of another year, charitable giving is likely top of mind. There are many ways to give back, each with unique benefits and considerations. One practical tool is the Individual Retirement Account (IRA).

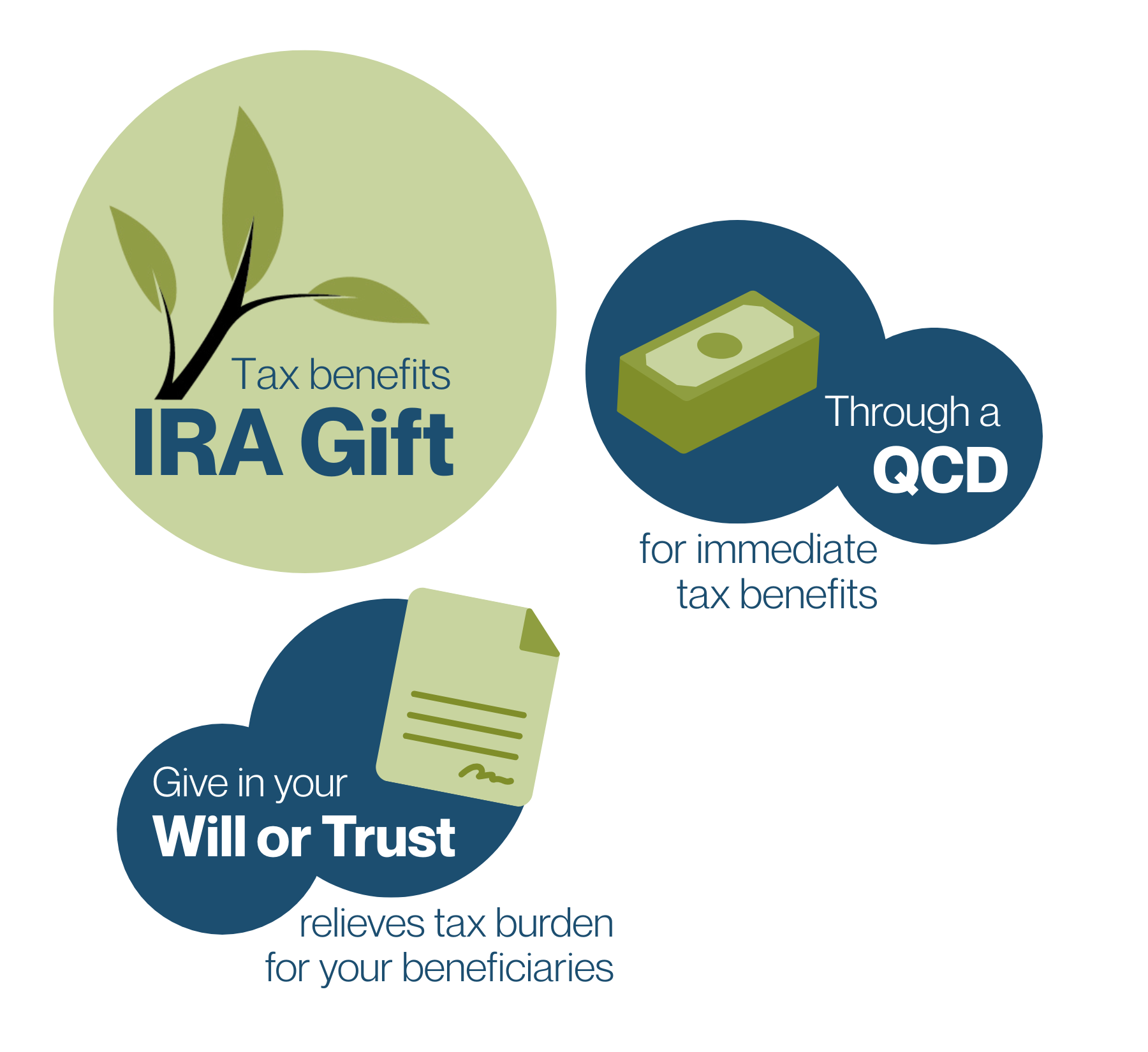

An IRA can be a powerful tool for supporting charitable causes both today and into the future. By making gifts directly from an IRA during your lifetime – or by designating a charity as the beneficiary in your estate plan – you can ensure that your giving has a meaningful impact while maximizing potential tax efficiency.

Qualified Charitable Distributions (QCDs): Giving Today

For those age 70 ½ and older, a Qualified Charitable Distribution is a powerful and faith-filled way to give. Through a QCD, you may direct up to $108,000 per year from your IRA straight to a qualified 501(c)(3) public charity, such as your parish, favorite ministry, other charitable organization. Instead of being taxed as ordinary income, these funds go directly to the mission you want to advance, allowing you to direct a distribution without increasing your taxable income. QCDs can be made from traditional IRAs as well as inherited IRAs and inactive SEP/SIMPLE IRAs.

Estate Giving with an IRA: Leaving a Legacy

While many donors already choose to support charitable organizations in their wills, using an IRA offers distinct advantages for building a legacy. In addition to supporting a charity’s immediate needs, an IRA gift can be directed to an endowment, ensuring that annual support continues for generations. This strategy can also result in tax benefits for both heirs and the charity. Key benefits include:

- When traditional IRA assets are distributed to heirs, income tax is generally applied based on the heir’s individual tax bracket. However, if distributed to a charity, the entire gift passes tax-free.

- Since a charitable organization does not pay income tax, 100% of the amount of the IRA distribution will directly benefit the charity.

- Your estate receives a charitable tax deduction for the gift, which may help offset estate tax obligations.

Giving With Purpose and Joy

By incorporating an IRA into your charitable plan – through QCDs now or through estate designations later – you can align your generosity with both your faith convictions and your potential tax benefits. Consider consulting with your attorney, tax advisor, or a charitable planning professional – such as those at charitable foundations – to determine the best approach for your philanthropic goals.

Submitted By: Lauren Denton, CPA

Managing Director, Forvis Mazars

Board President, Catholic Community Foundation of Northeast Indiana